- Most standard homeowners policies cover storm debris removal as part of a covered peril — but limits vary widely.

- Debris must usually be the result of damage to an insured structure to trigger coverage; yard-only debris often gets excluded.

- Document everything before cleanup begins — photos, videos, and itemized contractor estimates protect your claim.

- Illinois policyholders have the right to appeal a denied or underpaid claim through the Illinois Department of Insurance.

- Never sign a final settlement release until all debris removal costs — including hauling and disposal fees — are confirmed.

- Having a roll-off container sourced and ready before the adjuster arrives keeps cleanup moving and supports your documentation.

Yes, insurance claims for storm debris removal are covered under most standard homeowners policies — but only when the debris results from a covered peril that also damaged your property. Coverage amounts, limits, and exclusions differ from policy to policy, so knowing the details before a storm hits Peoria can mean thousands of dollars in the right direction.

📞 Need a Dumpster for Storm Cleanup in Peoria? Call Zap Dumpsters: (309) 650-8954

How Insurance Claims for Storm Debris Removal Actually Work

After a tornado, severe thunderstorm, or wind event hits a Peoria neighborhood, the debris left behind — fallen limbs, roof shingles, damaged siding, soaked drywall — adds up fast. The good news is that most homeowners insurance policies include debris removal as part of their “Additional Coverages” section, meaning you typically do not pay extra for it as a standalone benefit.[1]

The way it works is straightforward in theory: if a covered peril causes damage to your home and leaves debris behind, your insurer should cover the reasonable costs of removing that debris as part of restoring your property to its pre-loss condition. In practice, the key phrase is “covered peril.” Windstorms, hail, lightning, and tornadoes are standard covered perils under most Illinois homeowners policies. Flood damage, on the other hand, is typically excluded unless you carry separate flood coverage through the National Flood Insurance Program (NFIP) or a private flood policy.[2]

The Illinois Department of Insurance advises homeowners to contact their insurer as soon as possible after a storm, provide detailed documentation of all damage, and keep every receipt from emergency cleanup work — even temporary repairs like boarding up windows or covering a damaged roof.[3] These expenses are often reimbursable and help demonstrate to your adjuster that you took your duty to mitigate further damage seriously.

The Coverage Trigger: What Has to Happen for Debris Removal to Be Paid

Here is a distinction that trips up a lot of Peoria homeowners: insurance coverage for tree and branch removal often requires the debris to have actually struck or damaged a covered structure. A tree that falls cleanly into your yard without hitting your home, fence, or driveway may not trigger debris removal coverage at all — or may only be covered up to a low sublimit, often $500 to $1,000 per tree.[4] If that same tree falls on your roof, coverage activates under your dwelling protection and the debris removal benefit applies more broadly.

For storm damage that goes beyond falling trees — shingles torn from your roof, siding blown off a wall, structural materials scattered across your yard — the debris removal coverage is tied to your property damage claim. Your insurer pays reasonable cleanup costs as part of getting your property back to its original condition. Rabih Hamawi, a property insurance attorney, notes that policyholders should ask their insurance company for written confirmation that the loss location has been fully inspected before proceeding with cleanup, to avoid any later disputes over what was removed and why.[5]

What Gets Excluded: The Gaps You Need to Know About

Not all storm-related waste qualifies under a debris removal claim. Standard policies rarely cover stump grinding or removal of stumps that did not cause structural damage. They typically exclude debris that is located entirely on your property without having harmed an insured structure. Hazardous materials — contaminated soil, asbestos-containing materials disturbed by storm damage, chemical spills — require separate pollution liability coverage and are excluded under standard property forms.[6] Understanding these exclusions before you start cleanup prevents the frustrating situation of spending money on removal that your insurer later refuses to reimburse.

| Debris Situation | Typically Covered? | Coverage Type | Watch Out For |

|---|---|---|---|

| Tree falls on roof or fence | Yes | Dwelling / Other Structures | Per-tree sublimits ($500–$1,000) |

| Tree falls in yard only (no structure hit) | Often not covered | May have a low sublimit | Check policy language carefully |

| Roof/siding debris from windstorm | Yes | Dwelling (Coverage A) | Coverage limit exhaustion risk |

| Flood-soaked belongings and drywall | Only with flood policy | NFIP or private flood | Standard HO policy excludes flood |

| Tornado-damaged structure debris | Yes | Dwelling + Additional Coverages | Illinois: bundled under Wind & Hail |

| Stump removal / yard-only debris | Rarely covered | Typically excluded | Must be explicitly stated in policy |

Understanding Your Debris Removal Coverage Limits

Coverage limits are where insurance claims for storm debris removal get complicated. Most policies approach debris removal in one of two ways. The first is through your existing dwelling coverage (Coverage A): you use whatever dwelling limit is left over after structural repairs are paid to fund debris removal. The second is through an additional coverage extension — typically 5% of your Coverage A limit — that activates specifically for debris removal on top of your dwelling coverage.[1]

Here is a practical example. Say your Coverage A is $300,000. A tornado damages your home and repairs cost $200,000, leaving $100,000 in unused dwelling coverage. Your debris removal would come out of that $100,000. But if the storm caused $295,000 in repairs, nearly exhausting your dwelling limit, the 5% additional debris removal extension would provide up to $15,000 specifically for cleanup — protecting you from being left with almost nothing for hauling costs.[4]

For isolated incidents like a single tree hitting your home, the limits are much lower. Policies often cap per-tree removal at $500 to $1,000, regardless of how large the tree is or how much work it takes to remove it.[4] After a significant ice storm or tornado — both of which Peoria sees regularly — that sublimit can feel very small when you are looking at a yard full of broken limbs and storm waste.

ACV vs. Replacement Cost: Why It Matters for Your Debris Claim

The type of settlement your policy offers — Actual Cash Value (ACV) versus Replacement Cost Value (RCV) — does not directly apply to debris removal costs the same way it does to structural repairs or personal property. Debris removal reimbursement is generally paid based on the reasonable, documented cost of the cleanup work itself, not depreciated values. This means receipts, contractor invoices, and disposal fees are the foundation of your debris removal settlement, so keeping thorough records matters more here than anywhere else in the claim process.[3]

The Illinois Insurance Association notes that after a major disaster, most structural damage is settled on a replacement cost basis — but policyholders need to understand the difference before the storm hits, not after, so they can make informed decisions about their coverage levels and whether to add endorsements for additional debris removal protection.[7]

Watch: Insurance Claims for Storm Debris Removal — What You Need to Know

Filing Insurance Claims for Storm Debris Removal: Step by Step

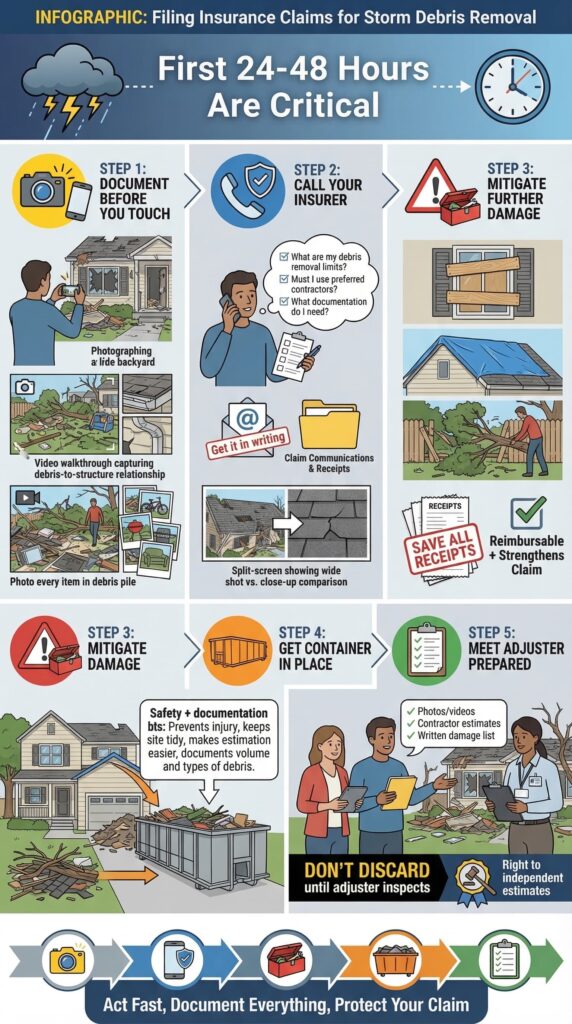

The steps you take in the first 24 to 48 hours after a storm can make or break your debris removal claim. Here is how to protect yourself from the moment the weather clears.

Step 1 — Document Before You Touch Anything

Walk your entire property and take wide-angle photos of every area affected, then close-up shots of specific damage points. Video walkthroughs are especially valuable because they capture the full scope and the relationship between fallen debris and damaged structures in a way that still photos sometimes miss. United Policyholders, a respected national policyholder advocacy organization, recommends photographing every recognizable item in the debris before anything is removed — particularly if your insurer may bring in a cleaning or salvage company, as their fees get deducted from your contents coverage.[1] The more thorough your documentation, the less room there is for disputes over what was there and what it cost to remove.

Step 2 — Call Your Insurer and Ask the Right Questions

Contact your insurance company as soon as possible. Illinois does not have a fixed deadline for filing property insurance claims, but policies typically require prompt notification — and delays can create complications if the insurer argues that further damage occurred because you waited.[8] When you call, ask three specific questions: What are my policy’s debris removal limits? Do I need to use a preferred contractor for cleanup? And what documentation do I need to keep for reimbursement?

Getting those answers in writing — even via email — protects you. The Illinois IDOI advises homeowners to keep a reference file with all claim-related communications, adjuster contact information, and every receipt from repairs or cleanup work throughout the process.[3]

Step 3 — Make Temporary Repairs and Mitigate Further Damage

You are expected to take reasonable steps to prevent additional damage — boarding up broken windows, tarping a damaged roof, removing debris that is actively damaging your home. In Illinois, failing to mitigate can give your insurer grounds to deny portions of your claim.[9] Keep every receipt from these emergency measures. They are reimbursable under your policy and demonstrating responsible action actually strengthens your overall claim position.

Step 4 — Get the Container in Place Before Full Cleanup Begins

One practical step that many Peoria homeowners overlook is getting a roll-off container sourced and positioned before the bulk of the cleanup work begins. Having a dedicated receptacle on-site means debris gets collected and contained in an organized way — which matters both for safety and for claim documentation. Zap Dumpsters Peoria helps homeowners and contractors source storm debris removal containers quickly after a severe weather event, giving you a central collection point for all the waste material that needs to go. If you are not sure how much capacity you will need, the guide on how to estimate the amount of debris from a storm walks through practical calculation methods for different storm types and debris categories.

Step 5 — Meet the Adjuster Prepared

When the insurance adjuster arrives, be present for the inspection. Bring your photo and video documentation, any contractor estimates you have collected, and a written list of all debris and damage you identified. The Illinois Insurance Association strongly advises against discarding any damaged items until the adjuster has examined them — even debris that seems obviously worthless may be important as physical proof of the loss.[7] If the adjuster’s estimate seems low or incomplete, you have the right to get independent repair and cleanup estimates from licensed local contractors to support your negotiation.

| Scenario | Standard Coverage (5% extension) | Debris Removal Endorsement Added |

|---|---|---|

| $200,000 Coverage A, $10,000 debris bill | Covered if dwelling limit not exhausted | Covered with higher separate limit |

| $200,000 Coverage A, dwelling repairs exhaust limit | Up to $10,000 (5%) for debris only | Broader protection, less out-of-pocket |

| Single tree falls on driveway | $500–$1,000 sublimit typical | Potentially higher depending on endorsement |

| Tornado causes major structural loss | May be insufficient for large cleanup | More likely to cover full removal costs |

When Insurance Claims for Storm Debris Removal Get Denied or Underpaid

Claim denials and low settlements happen. Understanding your options in Illinois is important so you do not walk away leaving money on the table.

Common Reasons Claims Are Rejected

Insurers most often deny or reduce debris removal portions of a claim when the debris did not result from damage to a covered structure, when the claimed cleanup costs exceed the policy sublimit, or when the damage is attributed to “wear and tear” rather than acute storm damage.[10] Documentation gaps — cleanup that began before the adjuster’s inspection, missing receipts, or a failure to notify the insurer promptly — can also weaken your position. The Illinois Consumer Protection Against Storm Chasers Act adds another layer of protection here: contractors are prohibited from waiving your deductible or negotiating on your behalf with the insurer, so working with reputable, licensed contractors and communicating directly with your adjuster is the right path.[7]

Your Rights Under Illinois Insurance Law

Illinois law requires insurers to respond to claims within a reasonable time frame, explain all coverage decisions clearly, and offer a fair settlement based on your policy terms.[10] If your insurer delays, denies, or significantly undervalues your claim, you have concrete options. You can file a formal complaint with the Illinois Department of Insurance (IDOI), which has authority to review whether the insurer acted in compliance with Illinois law — including bad faith claim handling provisions.[3] You can also hire a licensed public adjuster, who works on your behalf (typically for a percentage of the settlement) to negotiate a fair outcome. The IDOI requires all public adjusters in Illinois to be licensed, so verify credentials before signing anything.[3]

“When calculating the many costs involved in repairing or restoring property following a disaster, it is important to remember that debris removal costs are in addition to — rather than a part of — the value of the damaged property. Their impact on total loss amounts, and the coverage limitations in most standard policies, are frequently overlooked.”

— Sherri Walker, Director of Claims, Sentinel Risk Advisors[6]

Case Study: Getting the Settlement Right

A Peoria homeowner whose property sustained tornado damage in 2024 initially received an adjuster estimate that did not include the cost of removing a large section of collapsed fence and scattered roofing debris. By presenting detailed contractor quotes and photographs showing the debris in direct contact with the damaged structure, the homeowner was able to have those removal costs added to the final settlement — increasing the payout by over $2,800.

Settlement Management: How to Protect Your Debris Removal Payout

Getting the settlement right is just as important as filing the claim correctly. A few specific practices protect the value of your insurance claims for storm debris removal through the settlement phase.

Do Not Sign a Final Release Too Early

Illinois insurance regulations explicitly prohibit settlement checks from indicating “final payment” or “release of claim” unless policy limits have been reached or the claim is formally disputed.[3] This means if you accept a check and later realize a debris removal cost was not included, you can contact your insurer and request it be added — as long as coverage limits have not been paid out. Never sign a formal release or full settlement agreement until every debris removal expense, including hauling fees, disposal surcharges, and container rental costs, has been confirmed and documented.

Track Every Dollar of Debris Removal Expense

Every receipt, every invoice, and every contractor agreement related to debris removal strengthens your claim. Keep a dedicated folder — physical or digital — with documentation of all cleanup costs. This includes roll-off container rental invoices, which provide clear evidence of the volume and type of debris removed and that a professional waste management process was followed. When your insurer or their adjuster reviews your claim, organized and complete documentation dramatically reduces the chance of a dispute.

📞 Get a Storm Debris Container Near You in Peoria — Call (309) 650-8954

Finding Storm Debris Removal Support Near You in Peoria

After a major storm, Peoria and the surrounding communities within Peoria County can face high demand for cleanup resources. Acting quickly on both your insurance claim and your debris removal logistics pays off. The sooner you have containers on-site and documentation underway, the faster your property recovery moves — and the stronger your claim will be at settlement time.

Zap Dumpsters Peoria helps residential and commercial property owners source the right roll-off containers for storm cleanup across the Peoria area. Rather than waiting for municipal debris pickup schedules, having a dedicated container on your property lets you work on your timeline, keep debris organized by type for insurance documentation purposes, and move through the recovery process efficiently. Reach out directly to discuss sizing options and availability close to you.

—

Take Control of Your Claim and Your Cleanup

Filing insurance claims for storm debris removal does not have to be overwhelming. The process comes down to four things: knowing what your policy actually covers before a storm hits, documenting damage thoroughly before cleanup begins, communicating promptly and in writing with your insurer, and never settling until all your costs are on the table. Peoria homeowners have solid consumer protections under Illinois law, and resources like the IDOI and licensed public adjusters exist precisely for situations where a claim gets complicated. Start your cleanup with the right container in place, keep every receipt, and do not leave debris removal costs on the table.

Call Zap Dumpsters Peoria at (309) 650-8954 to get storm debris sourcing handled fast.

—

Insurance Claims for Storm Debris Removal FAQs

Are insurance claims for storm debris removal covered under a standard homeowners policy?

Insurance claims for storm debris removal are covered under most standard homeowners policies when the debris results from a covered peril — such as wind, hail, or a tornado — that also caused damage to an insured structure. Coverage is usually found in the “Additional Coverages” section and is subject to specific limits.

How much does homeowners insurance pay for storm debris removal?

Coverage amounts vary by policy, but most provide either a percentage of your dwelling coverage (commonly 5% as an additional extension) or a fixed dollar amount. For isolated fallen trees, many policies cap coverage at $500 to $1,000 per tree, which may not reflect actual removal costs after a major storm.

What documentation do I need to support insurance claims for storm debris removal?

You need wide-angle and close-up photos of all debris and damage before cleanup begins, video walkthroughs of affected areas, written contractor estimates for removal work, receipts for all cleanup expenses including container rentals, and written communication with your insurer throughout the claim process.

Can my insurance company deny a storm debris removal claim in Illinois?

Yes — common reasons for denial include debris that did not damage a covered structure, costs exceeding policy sublimits, or insufficient documentation. If your claim is denied unfairly, you can file a complaint with the Illinois Department of Insurance, which has authority to investigate bad-faith claim handling.

Does storm debris removal insurance cover stump removal or yard-only debris?

Storm debris removal insurance rarely covers stump grinding or debris that landed only in your yard without striking an insured structure — these are typically excluded under standard homeowners policy language. Some policies will cover stump removal only if it is explicitly stated as a covered benefit, so review your policy or ask your agent directly.

—

Insurance Claims for Storm Debris Removal Citations

- United Policyholders. “Debris Removal After a Disaster.” https://uphelp.org/claim-guidance-publications/debris-removal-after-a-partial-or-total-loss/

- Illinois Department of Insurance. “Disasters — What To Do Before, During and After.” https://idoi.illinois.gov/consumers/disasters.html

- Illinois Department of Insurance. “Post-Disaster Claims Guide.” https://idoi.illinois.gov/content/dam/soi/en/web/insurance/consumers/documents/claim-disaster-guide-7-23-2019.pdf

- Clovered. “Does Homeowners Insurance Cover Debris Removal?” https://clovered.com/does-homeowners-insurance-cover-debris-removal/

- Hamawi Law. “Debris Removal Coverage.” https://www.hamawilaw.com/post/debris-removal-coverage

- Sentinel Risk Advisors. “ABCs of Insurance Claims: D is for Debris Removal.” https://sentinelra.com/blog/abcs-of-insurance-claims-d-is-for-debris-removal

- Illinois Insurance Association. “Home Insurance for Spring Storm Damage.” https://www.illinoisinsurance.org/news-updates/home-insurance-spring-storm-damage

- ClaimSpot. “Illinois Guide to Property Insurance Claims: Deadlines & FAQs.” https://claimspot.com/insurance-claims/illionois-guide-insurance-claim-deadlines-faqs/

- Sill Public Adjusters. “Emergency Guide: Tornado Insurance Claims in Illinois and Indiana.” https://www.sill.com/latest-news/posts/emergency-guide-tornado-insurance-claims-in-illinois-and-indiana-march-2026/

- Huskie Exteriors. “Storm Damage Insurance Claims in Illinois: Expert Tips & Advice.” https://www.huskieexteriors.com/blog/p.260303003/understanding-the-insurance-claims-process-in-illinois/