Yes, you can save your house once it’s in foreclosure through several options including loan modifications, repayment plans, reinstatement, or bankruptcy filing. The key is acting quickly and working with your lender to find a solution before the foreclosure sale happens, as you typically have months to explore these alternatives.

Important Disclaimer: This article provides general information only and should not be considered financial advice. Every foreclosure situation is unique and complex. Before making any financial decisions regarding foreclosure prevention, consult with qualified professionals including your independent financial advisor, foreclosure attorney, and HUD-approved housing counselor who can evaluate your specific circumstances and provide personalized guidance.

Understanding Your Options Once Foreclosure Starts

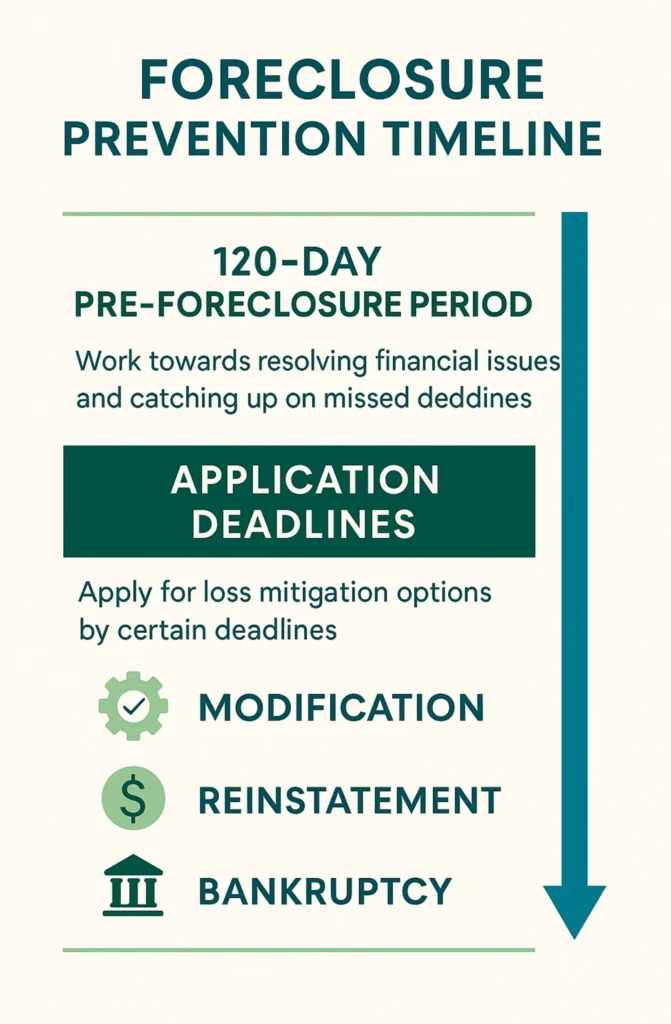

When foreclosure proceedings begin, many people think it’s too late to save their home, but that’s not true. Federal law requires lenders to wait at least 120 days before starting foreclosure, and even after it starts, you usually have several more months before the actual sale. This gives you time to explore various options that can stop the foreclosure and let you keep your house.

The most important thing is not to panic or ignore the situation. Lenders don’t actually want your house – they want their money back. This means they’re often willing to work with you to find a solution that avoids foreclosure, which is expensive and time-consuming for them too. Understanding what options are available helps you approach your lender with realistic proposals.

| Solution Type | Best For | Time Required | Success Rate |

|---|---|---|---|

| Loan Modification | Long-term payment problems | 30-90 days | Moderate – depends on income |

| Reinstatement | Temporary financial problems | Immediate if funds available | High – if you have the money |

| Repayment Plan | Few missed payments | Quick approval possible | High – with stable income |

| Chapter 13 Bankruptcy | Multiple debt problems | 60-90 days to file | High – stops foreclosure immediately |

Loan Modifications: Changing Your Mortgage Terms

A loan modification permanently changes your mortgage terms to make payments more affordable. This might include lowering your interest rate, extending the loan term, or even reducing the principal balance in some cases. Loan modifications work best when you can prove you have steady income but can’t afford your current payment amount.

The loan modification process typically takes 30-90 days and requires submitting a complete application with financial documents. Many homeowners wonder if they can simply pay back what they owe, but loan modifications often provide better long-term solutions than just catching up on payments.

Types of Loan Modifications Available

Several types of modifications exist depending on your loan type and situation. Interest rate reductions lower your monthly payment by reducing the rate you pay. Term extensions spread your balance over more years to reduce monthly payments. Principal forbearance temporarily reduces payments by deferring part of your balance to the end of the loan.

Government programs like HARP and FHA’s loss mitigation options provide standardized modification programs for eligible borrowers. These programs often have better terms than bank-specific modifications and include protections against foreclosure while your application is being reviewed.

Loan Modification Application Process

The application process requires detailed financial information including income statements, bank records, and a hardship letter explaining your situation. Federal law now protects you from “dual tracking” – where banks process foreclosure while considering your modification. If you submit a complete application at least 37 days before the foreclosure sale, they must review it before proceeding.

Working with HUD-approved housing counselors can improve your chances of approval. These counselors help you prepare applications, communicate with lenders, and understand your options at no cost. They know what lenders look for and can help present your situation in the best possible way.

Reinstatement: Catching Up on Missed Payments

Reinstatement means paying all missed payments, fees, and foreclosure costs in one lump sum to bring your loan current. This option works best if your financial problems were temporary and you now have access to enough money to catch up completely. Many homeowners use tax refunds, insurance settlements, or help from family to reinstate their loans.

The amount needed for reinstatement includes all missed payments plus late fees, attorney fees, and any costs the lender incurred during foreclosure proceedings. Request a “reinstatement quote” from your lender to get the exact amount needed and a deadline for payment. This quote is typically good for 10-15 days.

Sources of Reinstatement Funds

Common sources for reinstatement funds include borrowing from retirement accounts, family loans, sale of other assets, or refinancing through other lenders. Some people sell vehicles or take personal loans to raise the money needed. Government assistance programs sometimes provide emergency funds for mortgage reinstatement in qualifying situations.

Consider the long-term sustainability of reinstatement. If you can catch up but still can’t afford regular payments going forward, you might face foreclosure again within months. Combine reinstatement with budget changes or income increases to ensure you can maintain payments after reinstating.

Legal Right to Reinstatement

Many states and most mortgage contracts give you the legal right to reinstate your loan up until a certain point in the foreclosure process. This right typically expires shortly before the foreclosure sale, so timing is crucial. Some states allow reinstatement until five days before the sale, while others cut off this right earlier.

Understanding your reinstatement rights helps you plan timing and negotiate with lenders. Even if your legal right expires, lenders often accept reinstatement voluntarily since it gets them their money without the expense and uncertainty of foreclosure sales.

Need a dumpster to help clean up a foreclosure property?

Call Zap Dumpsters Peoria (309) 650-8954Repayment Plans: Spreading Out Past Due Amounts

Repayment plans let you catch up on missed payments gradually by adding extra amounts to your regular monthly payments over time. This option works well if you’ve only missed a few payments and can now afford your regular payment plus something extra each month to catch up on the arrears.

Typical repayment plans spread missed payments over 6-24 months depending on how much you owe and what you can afford. For example, if you owe $6,000 in back payments, you might pay an extra $300 per month for 20 months in addition to your regular payment. This approach is often easier to manage than coming up with a large lump sum.

Negotiating Realistic Payment Plans

Be honest about what you can afford when proposing repayment plans. Lenders prefer conservative plans you can actually complete over ambitious ones that set you up for failure. Include all your monthly expenses when calculating what extra amount you can realistically pay without creating new financial stress.

Some lenders offer “stepped” repayment plans where extra payments start small and increase over time as your income improves. Others prefer consistent extra payments throughout the plan period. Flexibility in structuring these plans makes them attractive options for many homeowners facing temporary financial difficulties.

Combining Repayment Plans with Other Solutions

Repayment plans can be combined with other foreclosure prevention strategies. Some people start with forbearance to stop immediate foreclosure pressure, then transition to repayment plans once their income stabilizes. Others use repayment plans as interim solutions while applying for loan modifications that provide permanent payment relief.

Consider how repayment plans affect your overall budget and long-term financial stability. While they help you catch up on missed payments, they also increase your monthly obligations temporarily. Make sure you can handle both regular and extra payments without falling behind again.

Bankruptcy as a Foreclosure Prevention Tool

Filing for bankruptcy immediately stops foreclosure through the “automatic stay” that prevents creditors from collecting debts or proceeding with foreclosures. Chapter 13 bankruptcy is particularly effective for saving homes because it provides a structured plan to catch up on mortgage payments over 3-5 years while keeping your house.

Chapter 13 works by creating a court-approved repayment plan that includes your missed mortgage payments along with other debts. You make monthly payments to a bankruptcy trustee who distributes money to creditors according to the plan. This approach can reduce other debts while protecting your home from foreclosure.

Chapter 13 vs Chapter 7 for Foreclosure

Chapter 13 bankruptcy is designed for people with regular income who want to keep their homes and catch up on payments over time. Chapter 7 only provides temporary foreclosure delay and doesn’t help you catch up on missed payments, making it less useful for saving homes. Choose Chapter 13 if your main goal is keeping your house.

Chapter 13 also allows you to “strip” second mortgages in some situations where your house is worth less than your first mortgage balance. This can eliminate significant monthly payments and make your overall housing costs more affordable. However, bankruptcy affects your credit and has other consequences that require careful consideration.

Timing Bankruptcy Filing Strategically

The timing of bankruptcy filing can significantly impact your foreclosure situation. Filing just before the foreclosure sale provides maximum delay and protection. However, earlier filing gives you more time to develop a feasible repayment plan and address other financial problems contributing to your situation.

Consult with bankruptcy attorneys who understand foreclosure timelines in your area. They can help you time the filing to maximize protection while ensuring you have realistic prospects for completing a successful Chapter 13 plan. Most bankruptcy attorneys offer free consultations to evaluate whether bankruptcy makes sense for your situation.

Working with Your Lender Effectively

Communication with your lender is crucial for successfully saving your home from foreclosure. Contact them as soon as you know you’ll have trouble making payments, rather than waiting until you’re already behind. Early communication shows good faith and gives you more options to work with.

Federal law requires lenders to assign you a single point of contact who can discuss your situation and help coordinate foreclosure prevention efforts. This person should be knowledgeable about your case and able to make decisions about workout options. If you’re not getting helpful responses, ask to speak with a supervisor or escalate through the lender’s complaint process.

Documenting All Communications

Keep detailed records of all conversations with your lender including dates, names of people you spoke with, and what was discussed. Follow up important conversations with written summaries sent to your lender. This documentation protects you if there are disputes about what was promised or agreed upon during the workout process.

Save all paperwork related to your foreclosure and workout attempts. This includes modification applications, hardship letters, financial documents, and any written correspondence. Having organized records makes it easier to work with attorneys or housing counselors if you need additional help.

Understanding Lender Incentives

Lenders have financial incentives to avoid foreclosure because it’s expensive and time-consuming for them. Foreclosure costs include legal fees, property maintenance, real estate commissions, and potential losses if the house sells for less than the mortgage balance. Understanding these costs helps you negotiate from a position of knowledge.

Government programs also incentivize lenders to offer modifications by providing financial payments for successful workouts. Many loans are owned by government-sponsored entities like Fannie Mae and Freddie Mac that have specific requirements for considering foreclosure alternatives before proceeding with sales.

Special Programs and Government Assistance

Various government programs provide additional options for saving homes from foreclosure. The Homeowner Assistance Fund provides up to $10 billion in state-run programs to help with mortgage payments and other housing expenses. USDA, VA, and FHA loans each have specific loss mitigation programs with generous terms for eligible borrowers.

State and local programs often provide emergency assistance, down payment assistance for refinancing, or mediation services to help negotiate with lenders. Some areas have foreclosure intervention services that provide comprehensive assistance throughout the process.

HUD Housing Counseling Services

HUD-approved housing counselors provide free services to help homeowners navigate foreclosure prevention. These counselors understand local programs, can help with paperwork, and often have established relationships with major lenders. They can also help you understand whether your situation is realistic for saving the home or if other alternatives might be better.

Housing counselors can also help you avoid foreclosure rescue scams that prey on desperate homeowners. Legitimate counseling is always free, while scam companies typically charge upfront fees for services that may not materialize. Work only with HUD-approved agencies that can be verified through the HUD website.

Military and Veteran Protections

Active military personnel and veterans have additional protections under the Servicemembers Civil Relief Act and VA loan programs. These include reduced interest rates during military service, extended foreclosure timelines, and specialized workout programs through VA loan technicians. VA loans offer some of the most generous loss mitigation options available.

Military families facing foreclosure should contact their base legal assistance office and VA regional loan centers for specialized help. These programs often have more flexible eligibility requirements and better terms than civilian programs, reflecting the unique challenges military families face with deployments and relocations.

Alternative Solutions When Traditional Methods Don’t Work

If traditional foreclosure prevention methods don’t work, several alternative approaches might still save your home or help you avoid foreclosure’s worst consequences. Short sales allow you to sell for less than you owe with lender approval, avoiding foreclosure while potentially preserving some equity and credit protection.

Deed in lieu of foreclosure involves voluntarily transferring ownership to the lender in exchange for debt forgiveness. While you lose the home, this option can provide more control over timing and may have less severe credit consequences than completed foreclosure. Some programs even provide relocation assistance.

Refinancing and Hard Money Options

Refinancing with other lenders might be possible even during foreclosure, especially if you have significant equity in your home. Hard money lenders charge higher rates but can close quickly when traditional lenders won’t approve loans. These short-term solutions can stop foreclosure while you arrange permanent financing or sell the property.

Private investors sometimes purchase homes subject to existing mortgages, allowing you to transfer ownership while avoiding foreclosure. These arrangements require careful legal review to ensure they’re legitimate and protect your interests. Be extremely cautious about any deals that seem too good to be true.

Family and Community Assistance

Family members sometimes provide loans or become co-borrowers to help save homes from foreclosure. Religious organizations, community groups, and local nonprofits occasionally have emergency assistance programs for housing costs. While these resources are limited, they’re worth exploring when other options aren’t sufficient.

Some communities have established foreclosure prevention funds or down payment assistance programs that can help with reinstatement or refinancing costs. Local housing authorities and community development organizations are good sources of information about these programs.

Timing and Legal Considerations

Understanding foreclosure timelines in your state helps you know how much time you have to work out solutions. Judicial foreclosure states typically provide more time but require court proceedings, while non-judicial states move faster but may offer fewer procedural protections. Knowing your timeline helps prioritize which solutions to pursue first.

Legal protections exist throughout the foreclosure process, including requirements for proper notice, opportunities to cure defaults, and procedures lenders must follow. Understanding how long you can stay in your house during various stages helps you plan effectively and avoid making premature decisions about moving out.

Working with Foreclosure Attorneys

Foreclosure defense attorneys can help you understand your rights, negotiate with lenders, and identify potential legal defenses to foreclosure. Many offer free consultations and can help even if you ultimately decide to work out solutions directly with your lender. Legal advice becomes particularly important if your lender isn’t responding to workout requests or you suspect improper procedures.

Some attorneys work on contingency or reduced fee arrangements for foreclosure defense, making legal help accessible even when money is tight. Attorney involvement often gets better responses from lenders and can help ensure you understand all implications of any agreements you’re considering.

Credit and Long-term Financial Impact

Successfully saving your home from foreclosure preserves your credit and housing stability. However, even successful loan modifications may be reported to credit bureaus as “partial payments” initially. Understanding these credit implications helps you make informed decisions about which foreclosure prevention options work best for your long-term financial health.

Compare the credit impact of different solutions when deciding which path to pursue. Completed loan modifications typically have less negative impact than foreclosure, bankruptcy, or short sales. However, the most important factor is often finding a solution you can actually sustain long-term rather than one that just delays foreclosure temporarily.

| Action Step | Immediate Priority | Timeline | Resources Needed |

|---|---|---|---|

| Contact lender immediately | High | Within days of first problem | Phone number, account information |

| Gather financial documents | High | Within first week | Pay stubs, bank statements, tax returns |

| Contact housing counselor | Medium | Within first month | HUD website to find local counselor |

| Submit loss mitigation application | High | Before 120 days past due | Complete financial package |

| Consider legal consultation | Medium | If lender not responsive | List of foreclosure attorneys |

Yes, you can definitely save your house once it’s in foreclosure, but success requires quick action and realistic assessment of your financial situation. The key is understanding that foreclosure is a process, not an immediate event, giving you time to explore options like loan modifications, repayment plans, reinstatement, or bankruptcy protection. Federal laws now provide better protections for homeowners seeking workout solutions, and lenders have financial incentives to avoid completed foreclosures. The most important steps are contacting your lender immediately, gathering necessary financial documents, and working with qualified housing counselors or attorneys who understand foreclosure prevention. While not every situation can be saved, many homeowners successfully keep their homes by acting quickly and pursuing appropriate solutions based on their specific circumstances and financial capabilities.

Remember: This information is for educational purposes only and does not constitute financial or legal advice. Foreclosure situations involve complex financial and legal considerations that vary by state and individual circumstances. Always consult with your independent financial advisor, qualified foreclosure attorney, and HUD-approved housing counselor before making decisions about foreclosure prevention strategies. They can provide personalized guidance based on your specific situation and help you understand the full implications of any course of action.

Can You Save a House Once It’s in Foreclosure FAQs

How long do I have to save my house once foreclosure starts?

You typically have several months to save your house once foreclosure starts, as the process usually takes 3-12 months depending on your state. Federal law requires lenders to wait 120 days before starting foreclosure, and then additional time passes before the actual sale occurs.

Can I get a loan modification after foreclosure has already started?

Yes, you can apply for loan modifications even after foreclosure starts, and federal law prohibits lenders from proceeding with foreclosure while reviewing complete modification applications. You must submit applications at least 37 days before any scheduled foreclosure sale for this protection.

Will filing bankruptcy immediately stop my foreclosure?

Yes, filing Chapter 13 bankruptcy immediately stops foreclosure through the automatic stay, and provides a court-supervised plan to catch up on missed payments over 3-5 years. Chapter 7 bankruptcy also stops foreclosure temporarily but doesn’t provide a way to catch up on missed payments long-term.